Something notable happened at the end of 2025. Multiple independent voices, including investors, builders, and researchers, arrived at the same conclusion about onchain vaults. There was no coordination, but the reasoning converged as market structure matured, vault productization accelerated, and distribution began to take shape.

Below is a snapshot of those views.

Growth expectations

Several forecasters are landing in a similar range. Roughly 2 to 3x growth in vault AUM over the next 12 months.

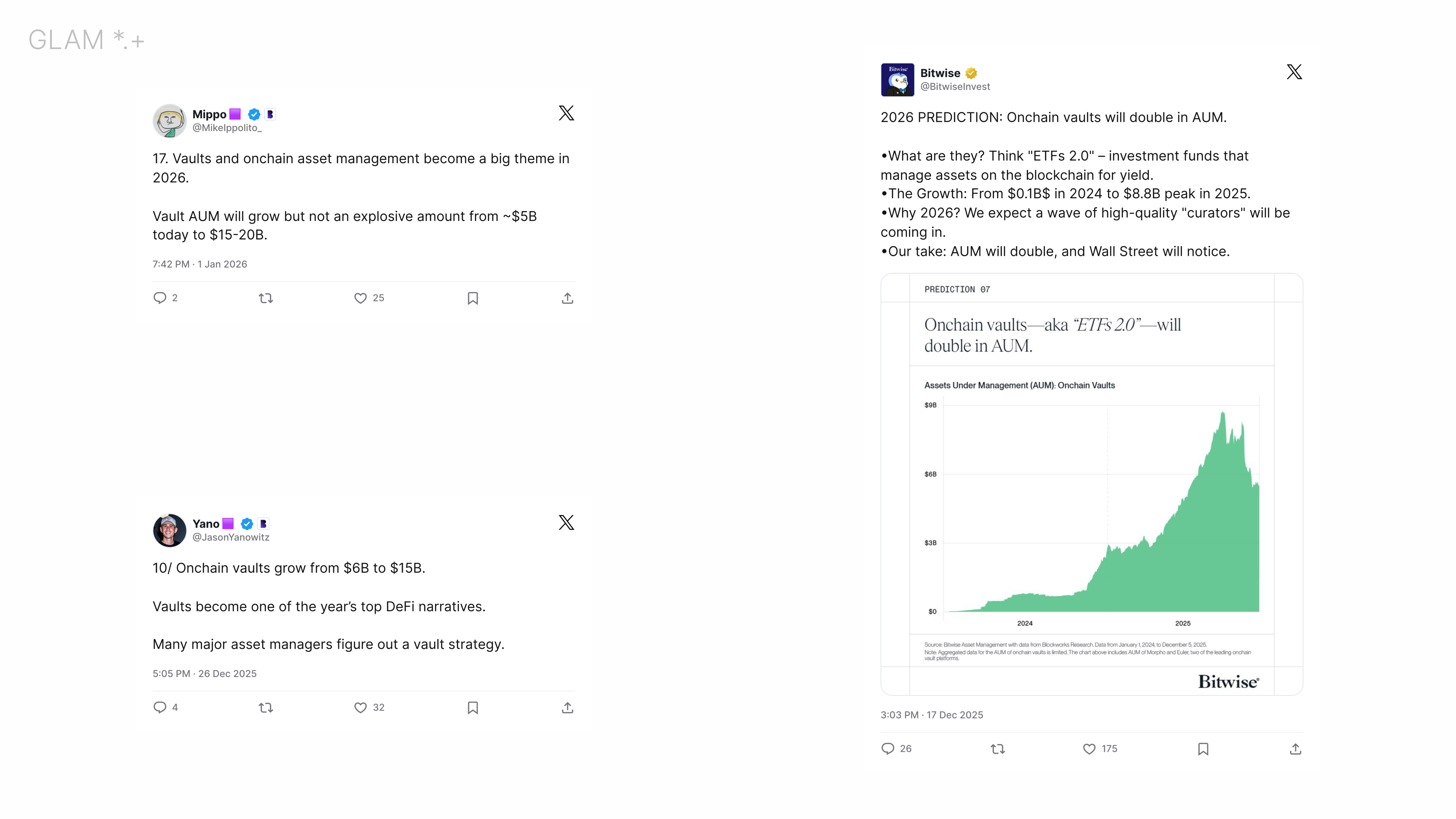

Bitwise: “AUM will double, and Wall Street will notice.”

Jason Yanowitz: “Onchain vaults grow from $6B to $15B. Vaults become one of the year’s top DeFi narratives. Many major asset managers figure out a vault strategy.”

Mike Ippolito: “Vaults and onchain asset management become a big theme in 2026. Vault AUM will grow but not an explosive amount from roughly $5B today to $15 to $20B.”

When independent estimates cluster around the same outcome, it is a signal worth tracking.

Institutional distribution is becoming specific

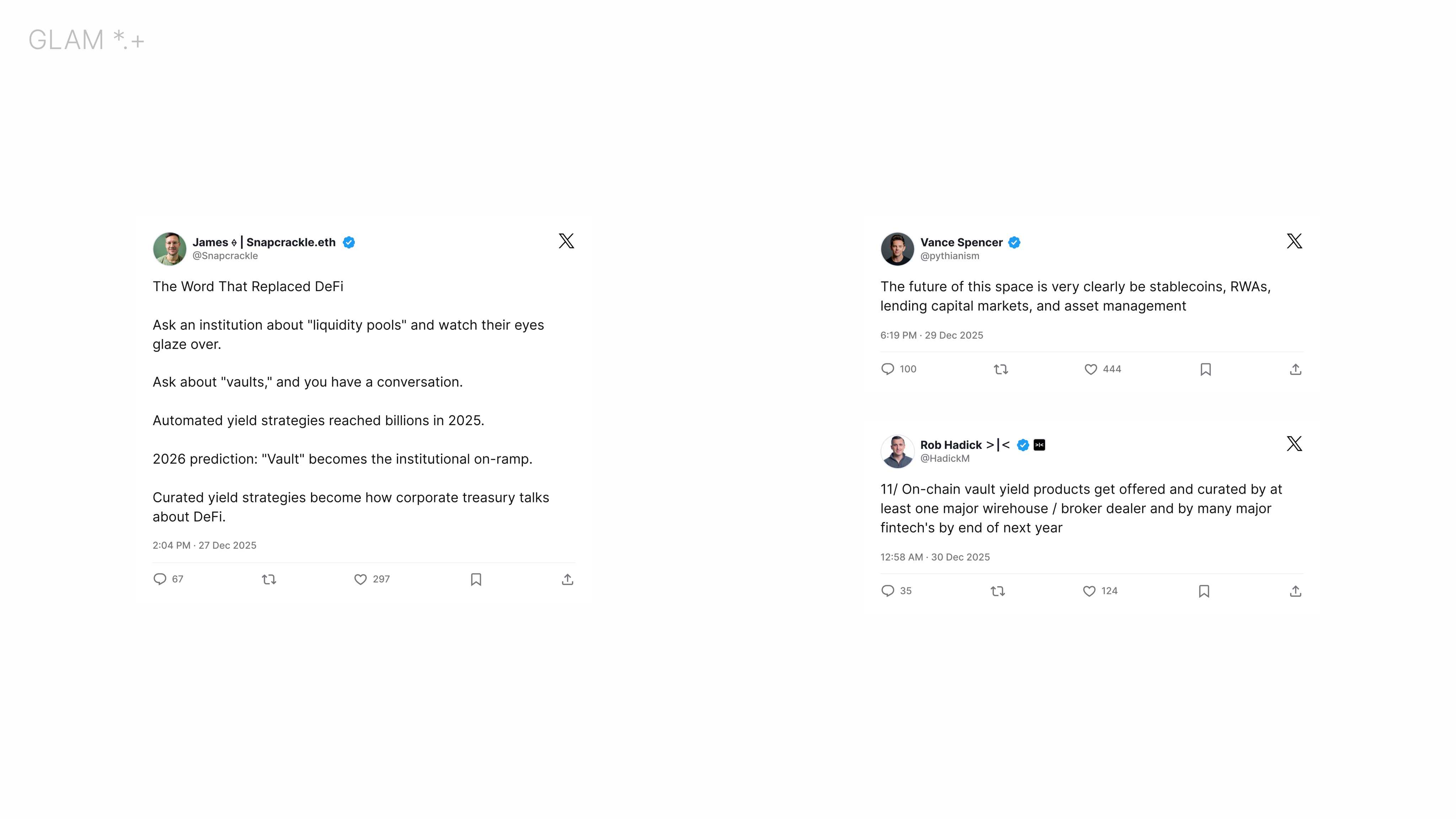

Institutional participation has been discussed for years. What is changing is specificity, particularly around distribution channels, not just adoption.

James Smith: “2026 prediction: ‘Vault’ becomes the institutional on-ramp.”

Rob Hadick: “On-chain vault yield products get offered and curated by at least one major wirehouse or broker dealer and by many major fintechs by end of next year.”

Vance Spencer: “The future of this space is very clearly stablecoins, RWAs, lending capital markets, and asset management.”

Predictions referencing wirehouses and broker dealers are not abstract. They imply product packaging, compliance processes, and a path to scale through existing financial infrastructure.

Who wins

Two themes recur. Growth in the number of managers, and a competitive gap between regulated incumbents and faster, more flexible teams.

Kyle Samani Noticed an “explosion of vault managers” at Breakpoint 2025, which took place in December in Abu Dhabi.

Ryan Connor: “Major TradFi names enter the vaults market. But, held back by regulation and internal red tape, they cannot compete with crypto native teams. Their TVL meaningfully lags crypto native incumbents, because their constrained opportunity set inherently limits yield generation.”

Even with strong brands and distribution, large institutions often face narrower mandates, longer product cycles, and stricter permissible assets. That creates a time bound advantage for teams that can iterate quickly while maintaining operational rigor.

The open question is not whether institutions participate. The question is how long the gap persists, and which platforms are built to serve both segments without compromising on controls.

What unlocks the next phase

Growth projections assume the product layer matures. Two perspectives frame what that means in practice.

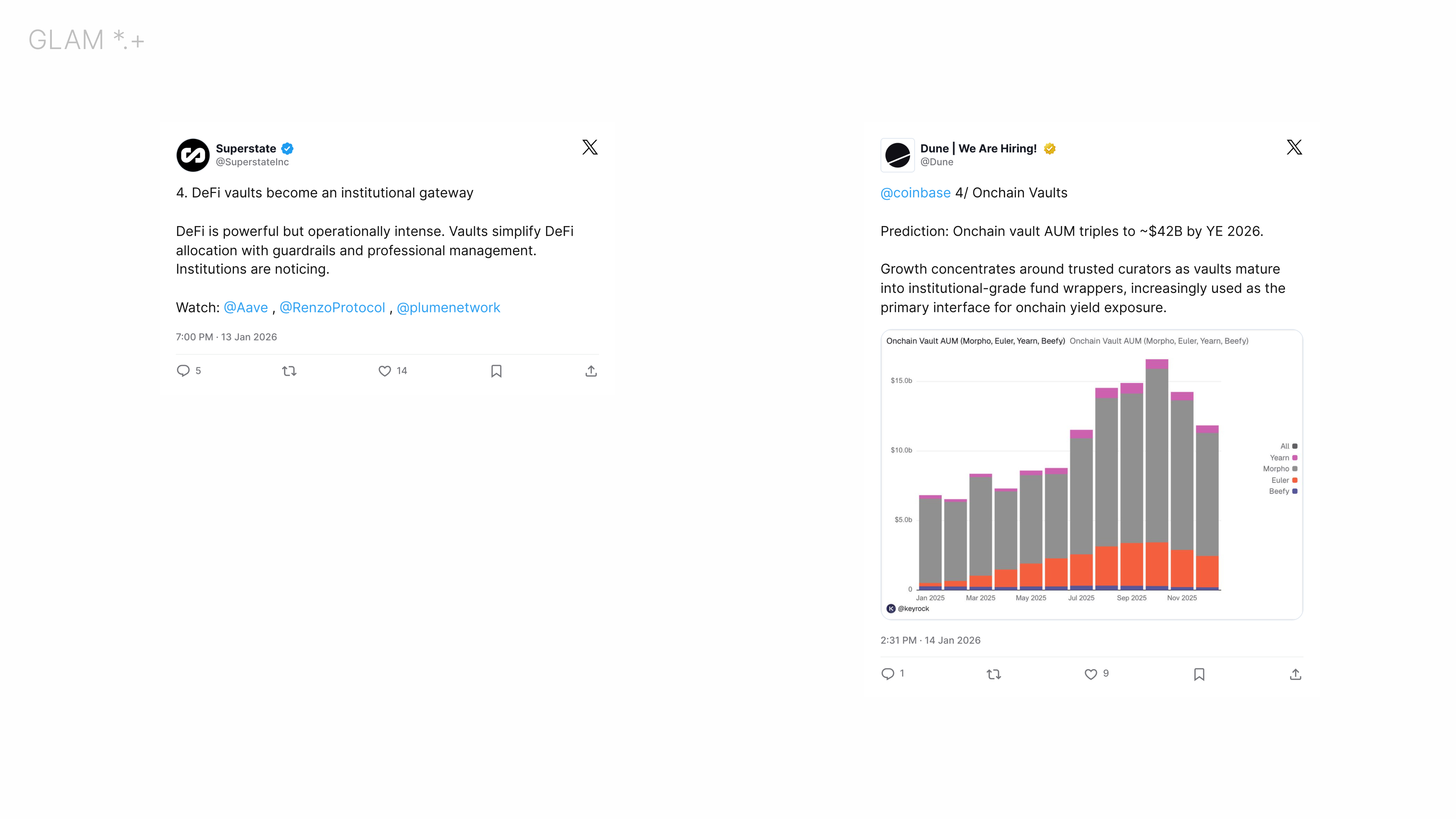

Superstate: "DeFi vaults become an institutional gateway. DeFi is powerful but operationally intense. Vaults simplify DeFi allocation with guardrails and professional management. Institutions are noticing."

Dune / Keyrock: "We don't see the next phase of vault growth coming from just higher APY potential, but rather enhanced process and better controls. As the vault product layer matures, it also becomes the natural interface for disclosures, reporting, suitability, and distribution partnerships, which is exactly what broker-dealers and wealth platforms need before they can offer these products confidently."

The pattern is clear. Vaults abstract complexity for institutions, but only if the underlying infrastructure meets their operational requirements. Higher yields alone do not unlock distribution. Controls, transparency, and compliance readiness do.

Implications

Vaults are moving from a niche product category to a core market primitive for onchain asset management. The thesis is no longer speculative. Independent forecasts converge, distribution channels are taking shape, and the requirements for institutional adoption are becoming explicit.

The remaining work is execution. Standardization, risk controls, monitoring, permissions, reporting, and integrations that allow vault strategies to scale safely.

For GLAM, this is the focus. The market is past the "does this matter" phase. The next phase is "who can operate it reliably at scale."